research

FO Analysis: The Silence Premium.

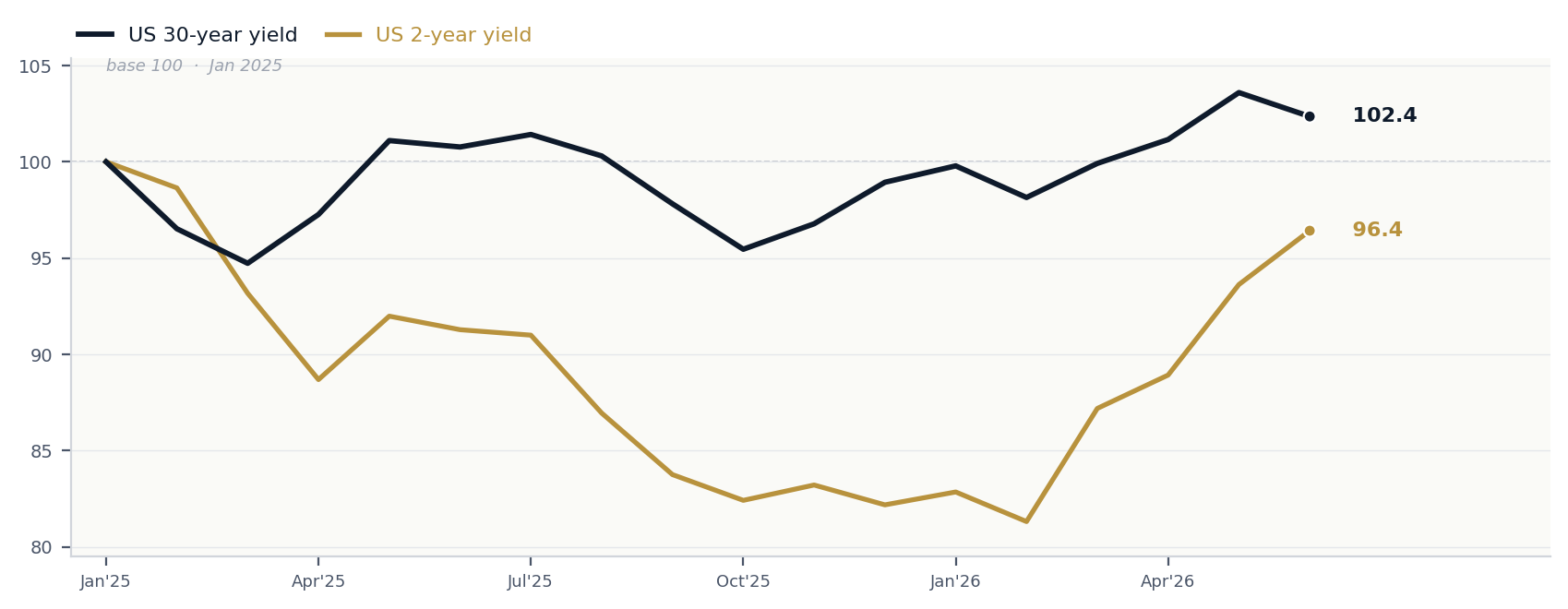

For fifteen years the Federal Reserve's most powerful tool was not a rate. It was a sentence. By telling the market what it would probably do next, through the dot plot, through calibrated statement language, through a reaction function everyone could read, the Fed suppressed the one thing long-dated bonds charge the most for: uncertainty about the path. The new chair is moving to take that tool away. Reporting through the week describes a push to scale back forward guidance and to diminish the dot plot, with investors warning the change could lift US borrowing costs. The desk reads it the same way, and names the mechanism plainly. When the central bank stops guiding, the market must price the path itself, and term premium comes back. That is not a small communications story. It is a new structural force acting on the exact part of the curve our floor thesis is built on. The long end is already held up by the deficit, the refunding calendar and a thinning foreign bid. A guidance withdrawal stacks a communication premium on top of those, and the tape already shows its fingerprint: long yields firm while inflation expectations sit still, which means the move is real rate and term premium, not an inflation scare.

The Data Spine

| DATA POINT | AS OF / NOTE | |

|---|---|---|

| US 30-year yield | ~4.94% | the floor, holding · the part of the curve a guidance withdrawal acts on |

| US 2-year yield | ~4.21% | anchored · no cut priced at the new chair's debut hold |

| US 10-year yield | ~4.49% | the belly holds with the long end |

| 2s30s spread | ~+70bp | steep · term premium at the long end, the premium story on the tape |

| Fed funds target (upper) | 3.75% | held at the 16 to 17 June FOMC, the new chair's first meeting |

| 10-year inflation breakeven | ~2.21% | contained · the yield rise is real rate and term premium, not inflation |

| HY OAS | 2.66 | near cycle-tight · no credit stress beneath the long end |

| DXY | ~101.4 | fresh year high · higher US real yields, the relative winner |

| Gold (spot) | ~$4,090 | bid · the fiscal and real-asset hedge, trading the dollar not the war |

| EUR/USD | ~1.1354 | through the year low on the dollar bid |

| USD/JPY | ~161.4 | yen weak · the foreign-bid pressure on US duration persists |

Market levels: Treasury yields and the high-yield spread are the latest official FRED prints as of 18 to 24 June 2026, pending final H.15 updates; FX, the dollar index and gold are live indicative reads from the morning tape of 24 June. Not official closes.

Recent Calls · Scored Against the Tape

What Ratified. What Is Advancing.

The desk publishes its reads before the data, dated, and scores them in public afterwards. This note does not start a new franchise. It adds the next chapter to the one the desk has run since early May: the long end is owned by term premium and supply, and a quieter Fed is about to add to both.

| Call | Ratified | What happened |

|---|---|---|

| The Long Bond Disconnect (8 May): term premium and supply own the long end, not the Fed path. | YES | The founding rates call, and the spine of this note. The long end has held its floor through every test since: data, a war, and a ceasefire. This note adds the next chapter, a communication premium, to the same term-premium story. |

| New Chair. Same Floor. (15 Jun Brief): Warsh inherits a floor he cannot talk down, held up by forces outside the Fed. | ADVANCING | The thesis was that the new chair cannot talk the floor down. This note sharpens it: he is not only unable to lower it, his framework change is set to push it higher. Same floor, and now a new leg under it. |

| The Buyers Go Home. (16 Jun Premium): the floor is a bid problem, a thinning foreign buyer base meeting a heavy calendar. | ADVANCING | The bid leg of the floor is intact: Japan tightening, the yen near 161, the foreign bid still stepping back. The silence premium stacks on top of that bid problem, not in place of it. Two structural forces, one long end. |

| The Floor Held. Again. (10 Jun Premium): the 30-year holds its tests because the level is structural, not data-driven. | YES | It held the hot jobs print, the soft core and the broadening PPI. Since then it has held the ceasefire and the oil decline too. The floor is structural, which is exactly why a new structural force, guidance withdrawal, matters more than another data point. |

| The War Is Over. The Floor Isn't. (19 Jun Brief): peace did not lower the floor; oil fell and the 30-year did not. | YES | Confirmed further this week: the US issued sweeping Iran oil sanctions waivers and the Strait reopened, oil fell again, and the 30-year still sits near 4.94. Peace did not buy a Treasury, and now a quieter Fed will not either. |

The full desk read continues below for Premium subscribers: the Regime Dashboard, the three-path Scenario Map with invalidation, the framework change and the mechanism in full, the conditionality that makes the premium large here, the cross-asset breakdown, how the desk expresses it, the FO Tactical View, the Trader's Checklist, the glossary, and the Premium PDF.

| FO Premium Edition |

| Read the full silence-premium verdict. |

| The new chair is moving to diminish the dot plot and forward guidance, the apparatus that suppressed term premium for fifteen years. The desk reads it the same way the market is starting to: a Fed that stops guiding hands the long end back the uncertainty it charges for, and term premium comes back. The 30-year holds near 4.94% while the 10-year breakeven sits still near 2.21%, so the move is real rate and premium, not an inflation scare. Premium subscribers receive the full desk read: the framework change, the mechanism, the conditionality that makes the premium large here, the Regime Dashboard scorecard, the three-path Scenario Map with explicit triggers and invalidation, how the desk expresses it, the FO Tactical View, the Cross-Asset Breakdown, the Trader's Checklist, and the downloadable editorial-grade PDF. |

| What Premium Includes |

| ✓The full structural chain: the framework change, the mechanism that connects a quieter Fed to a higher long end, the conditionality that makes the premium large here, the cross-asset confirmation, and the regime. |

| ✓Confirmed / Observed / FO Inference / FO Risk Scenario labels throughout, separating sourced facts from interpretation. |

| ✓The Regime Dashboard scorecard: 10 cross-asset signals colour-coded RED / AMBER / GREEN. |

| ✓The three-path Scenario Map (Path A the premium builds / Path B the chair stays legible / Path C a volatility shock above 5.20) with explicit triggers and invalidation. |

| ✓The five sections in full: the framework change, why guidance was a premium suppressant, where the silence premium stacks, the cross-asset read, and the regime. |

| ✓How the Desk Expresses It: the cleanest ways to carry the view, from the curve steepener to long-end rate volatility. |

| ✓The FO Tactical View matrix: directional reads across the 30-year, 2-year, 2s30s, rate volatility, DXY, gold, HY OAS and the AI complex. |

| ✓The Cross-Asset Breakdown: instrument-by-instrument reads on the 30-year, 2-year, 2s30s, DXY, gold and HY OAS. |

| ✓The Trader's Checklist: a tickable one-page sheet, with the rate-volatility and auction tells that confirm or break the thesis. |

| ✓The glossary: plain-language definitions of forward guidance, the dot plot, term premium, the silence premium and the rest. |

| ✓Editorial-grade downloadable PDF, desk-formatted for print, with the curve chart, the nominal-versus-breakeven chart and the credit cross-check. |

| Recently Published · Premium Only |

| 16 June 2026The Buyers Go Home.The floor under the long end is a bid problem, not a war premium: a thinning foreign buyer base meeting a heavy refunding calendar. |

| 10 June 2026The Floor Held. Again.The 30-year held its tests through a hot jobs print and a soft core because the level is structural, not data-driven. |

| 15 June 2026New Chair. Same Floor.The new chair inherits a floor he cannot talk down, held up by forces outside the Fed's gift. |

| 8 May 2026The Long Bond DisconnectFront-end cut pricing barely moved the 30-year. Term premium is reasserting at the long end. |

| Subscribe to FO Premium |

| Editorial-grade macro research, written for sophisticated readers. Notes land when the data warrants. |

Receive every report at the source.

The FO Brief is free. Premium delivers the full archive. Institutional includes analyst Q&A.

Subscribe →