research

FO Analysis: The Bid Comes Home.

The market has decided what the new Federal Reserve chair is. At the June meeting the dots turned hawkish, the median moving up and nine of eighteen officials projecting a hike, and the chair is withdrawing forward guidance, which lifts the premium investors demand to lend long. That is a tightening hand, and the desk mapped it this morning in The Silence Premium. But it is one hand, and the market is pricing only it. The same chair, through the same Fed, is easing the plumbing. A leverage rule that penalised banks for holding Treasuries was recalibrated in a final rule effective the first of April, freeing, by the agencies' own analysis, the largest banks' Treasury-intermediation capacity from near zero to roughly $1.1 trillion at their depository units and $2.1 trillion at their broker-dealers, with the explicit purpose of removing the leverage penalty on holding Treasuries. And on the nineteenth of March the agencies re-proposed the Basel III endgame in a form that, on their own estimate, modestly lowers system capital, the reversal of a 2023 plan that would have raised the largest banks' capital by roughly a fifth. Comments closed on the eighteenth of June. The final rule is now the next regulatory event. This is a stealth easing of financial conditions, delivered through capital rules rather than rate cuts, and it reopens a question our floor work deliberately left one-sided. The foreign bid is leaving. The domestic bank bid is being freed to come home.

The Data Spine

| DATA POINT | AS OF / NOTE | |

|---|---|---|

| eSLR relief (GSIBs) | ~0 to $1.1T / $2.1T | Treasury-intermediation capacity freed, depository / broker-dealer · Tier 1 req. down ~$13B (HC), ~$219B (depo) · final rule eff. 1 April 2026 |

| Basel III endgame, 2026 re-proposal | net lower capital | proposed 19 March · agencies estimate a modest system decrease · comments closed 18 June |

| The capital arc | +19% to net cut | 2023 plan (~+19% GSIB) to 2024 re-proposal (~+9%) to 2026 (net decrease) |

| Advancing vote | 6 to 1 | the lone dissent warned the changes weaken post-crisis safeguards |

| Operational risk coefficients | 12 / 15 / 18% | the calibration the industry fought as overstated for US banks |

| Fed funds target (upper) | 3.75% | held 17 June · the new chair withheld his own dot |

| June dot plot | median 3.8% | hawkish · 9 of 18 project a hike, only 1 a cut · the brake |

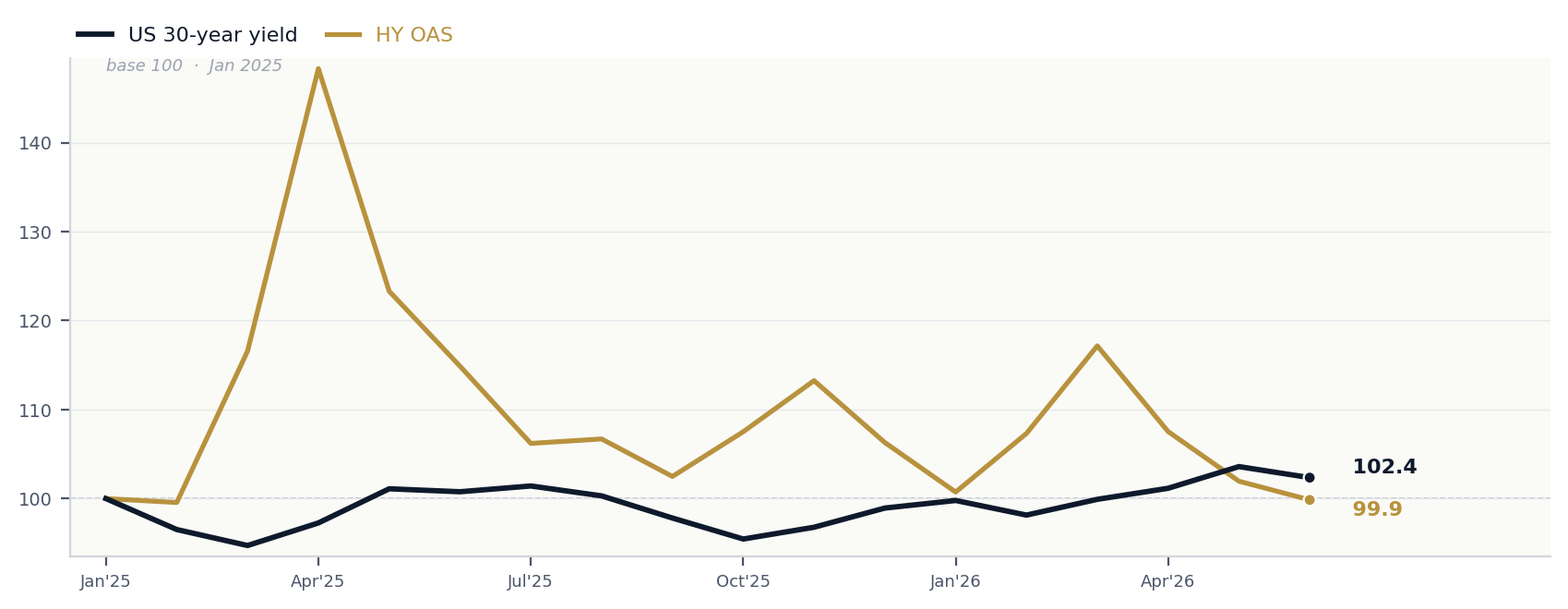

| US 30-year yield | ~4.90% | the floor · the relief reaches it only partly, see the body |

| HY OAS | 2.72 | near cycle-tight · the easing already in the credit channel |

| Bank equities | regionals +10.3% YTD | the bank index +7.8% YTD, both +3.8% on the month · rising into higher rates |

| DXY | ~101.4 | fresh highs · an easing through balance sheets does not soften the dollar like a pivot would |

| Treasury (Bessent) | backs the bid | Sec. backs eSLR reform on the same logic; buyback overhaul expands long-end ops + counterparties; bill-heavy issuance |

| Bessent 3-3-3 (reaffirmed 24 Jun) | 3% / 3% / +3mbpd | growth by year-end, deficit-to-GDP, oil · the aspirational floor-easer, war-and-tariff challenged |

| 2-year auction (23 Jun) | 2.64 b/c | slightly above the 2.61 ten-auction average · indirect just over half · the front-end bid, on cue |

| 5-year auction (24 Jun) | 2.35 b/c, 0.7bp tail | cleared but soft · indirect 61.6% (from 74.9%), direct 25.5% (from 12.3%) · foreign out, domestic in |

Market levels: Treasury yields and the high-yield spread are the latest official FRED prints as of 18 to 24 June 2026, pending final H.15 updates; FX, the dollar index, gold and bank-equity levels are live indicative reads from the morning tape of 23 to 24 June. Regulatory figures are the agencies' own estimates. Not official closes.

Recent Calls · Scored Against the Tape

What Ratified. What Is Advancing.

The desk publishes its reads before the data, dated, and scores them in public afterwards. This note completes a pair. The Silence Premium mapped the brake this morning; this maps the accelerator. And it adds the missing other half to the bid thesis the desk has run since May: the floor is a bid problem, and a domestic bank bid is being freed to come home as the foreign bid departs.

| Call | Ratified | What happened |

|---|---|---|

| The Buyers Go Home. (16 Jun Premium): the floor is a bid problem, a thinning foreign buyer base meeting a heavy calendar. | ADVANCING | This note adds the missing other side. The foreign bid is still leaving, but a domestic bank bid is being freed to come home through capital and leverage relief. The bid leg of the floor now has two-way news, which is exactly the nuance the framework needed. |

| The Silence Premium. (23 Jun Premium, companion): withdrawing guidance lifts term premium, the brake. | NEW | Published this morning. This note is its mirror: the same chair easing the plumbing while tightening the signal. Read together, they are the regime, a Fed running the brake and the accelerator at once, and a market pricing only the brake. |

| The Long Bond Disconnect (8 May): term premium and supply own the long end. | YES | Holding, and it disciplines this note's own optimism. Even a returning bank bid skews short, so the 30-year still needs term premium to turn before the floor eases. The accelerator reaches the front and the plumbing first, the long end last if at all. |

| New Chair. Same Floor. (15 Jun Brief): Warsh inherits a floor he cannot talk down. | ADVANCING | Sharpened. He is not talking the floor down, he is easing the plumbing beneath it. Same floor, and now a cross-current under it: a capital-freed bid pulling one way against the supply and foreign-bid forces pulling the other. |

| The Last AAA (19 May): a contracting pool of forced, mandate-driven buyers lifts the long end. | ADVANCING | The first force pushing the other way. Capital and leverage relief partially re-enlists US banks as Treasury buyers, slowing the contraction of the buyer base. It does not reverse it, the foreign bid still dominates the long end, but it is the first genuine offset the desk has logged. |

The full desk read continues below for Premium subscribers: the Regime Dashboard, the three-path Scenario Map with invalidation, the two levers and the mechanism in full, where the returning bid reaches the floor and where it does not, the two-arm Fed-and-Treasury bid thesis, the cross-asset breakdown, how the desk expresses it, the FO Tactical View, the Trader's Checklist, the glossary, and the Premium PDF.

| FO Premium Edition |

| Read the full accelerator-and-brake verdict. |

| The market is pricing one hand. The June dots turned hawkish and the new chair is withdrawing guidance, the brake mapped in the companion note. But the same Fed is easing the plumbing. A leverage rule that penalised banks for holding Treasuries was recalibrated, freeing the largest banks' Treasury-intermediation capacity from near zero to roughly $1.1 trillion at their depository units, and the Basel III endgame was re-proposed to cut system capital rather than raise it. That is a stealth easing of financial conditions through capital rules, and it frees a domestic bank bid to come home as the foreign bid leaves. Premium subscribers receive the full desk read: the two levers, the mechanism, where the bid reaches the floor and where it does not, the two-arm Fed-and-Treasury bid thesis, the Regime Dashboard scorecard, the three-path Scenario Map with explicit triggers and invalidation, how the desk expresses it, the FO Tactical View, the Cross-Asset Breakdown, the Trader's Checklist, and the downloadable editorial-grade PDF. |

| What Premium Includes |

| ✓The full structural chain: the two capital levers, the mechanism that turns a line in a capital rule into a trillion-dollar balance-sheet question, where the returning bid reaches the floor and where it does not, the cross-asset confirmation, and the regime. |

| ✓Confirmed / Observed / FO Inference / FO Risk Scenario labels throughout, separating sourced facts from interpretation. |

| ✓The Regime Dashboard scorecard: 11 cross-asset signals colour-coded RED / AMBER / GREEN, including the Treasury debt-management signal. |

| ✓The three-path Scenario Map (Path A the accelerator engages / Path B the bid reaches the long end / Path C the releveraging tail) with explicit triggers and invalidation. |

| ✓The eSLR recalibration and the Basel III endgame re-proposal mechanics in full, separating what is finalised from what is still a proposal. |

| ✓The two-arm Fed-and-Treasury bid thesis: the Treasury Secretary's backing of eSLR reform and the buyback overhaul that supplies the duration the banks will not. |

| ✓The 2-year and 5-year auction reads, the front-end bid on cue and the foreign-to-domestic rotation in the composition. |

| ✓The FO Tactical View matrix: directional reads across bank equities, the 30-year, the 2-year, 2s30s, HY OAS, DXY, gold and Treasury functioning. |

| ✓The Cross-Asset Breakdown: instrument-by-instrument reads on bank equities, the 30-year, the front end and repo, HY OAS, the dollar and gold. |

| ✓How the Desk Expresses It: the cleanest ways to carry the two-handed view, from long banks against long-duration growth to the where-the-bid-lands curve trade. |

| ✓The Trader's Checklist: a tickable one-page sheet, with the auction and stress-test tells that confirm or break the thesis. |

| ✓The glossary: plain-language definitions of the eSLR, the Basel endgame, Treasury-market intermediation, the domestic bank bid and the rest. |

| ✓Editorial-grade downloadable PDF, desk-formatted for print, with the credit-channel chart and the curve chart. |

| Recently Published · Premium Only |

| 23 June 2026The Silence Premium.The companion note. The same chair easing the plumbing while withdrawing guidance: a Fed running the brake and the accelerator at once. |

| 16 June 2026The Buyers Go Home.The floor under the long end is a bid problem: a thinning foreign buyer base meeting a heavy refunding calendar. This note adds the other side. |

| 15 June 2026New Chair. Same Floor.The new chair inherits a floor he cannot talk down. He is not talking it down, he is easing the plumbing beneath it. |

| 8 May 2026The Long Bond DisconnectFront-end cut pricing barely moved the 30-year. Term premium and supply own the long end, and discipline this note's optimism. |

| Subscribe to FO Premium |

| Editorial-grade macro research, written for sophisticated readers. Notes land when the data warrants. |

Receive every report at the source.

The FO Brief is free. Premium delivers the full archive. Institutional includes analyst Q&A.

Subscribe →