Why the 54–45 Confirmation Is a Regime Change the Market Has Priced as a Headline

Free Brief + Premium Edition Below

DESK

Global Macro | Fed Policy, Rates & Cross-Asset

CONVICTION

High — structural Fed-policy reprice ahead

HORIZON

1 – 3 quarters

DATE

15 May 2026

CLASSIFICATION

Free Brief + Premium | FO Research

Executive Summary

Regime Change Priced as a Personnel Headline

On 13 May 2026 the United States Senate confirmed Kevin Warsh as Federal Reserve Chair by a 54 to 45 vote — the narrowest Fed-chair confirmation in modern record. The same morning, the Bureau of Labor Statistics reported April Producer Price Index final demand at +1.4% month-on-month and +6.0% on the year. Jerome Powell’s term ends today. Chair Warsh takes office with a 5% 30-year yield, an OIS curve still pricing year-end cuts the confirmation record opposes, and a pipeline-inflation print landed four trading days before he assumes the chair.

The market is treating the confirmation as a personnel headline. The data is treating it as a regime change. The two readings will reconcile — through 17 June communication or through repricing in the meantime.

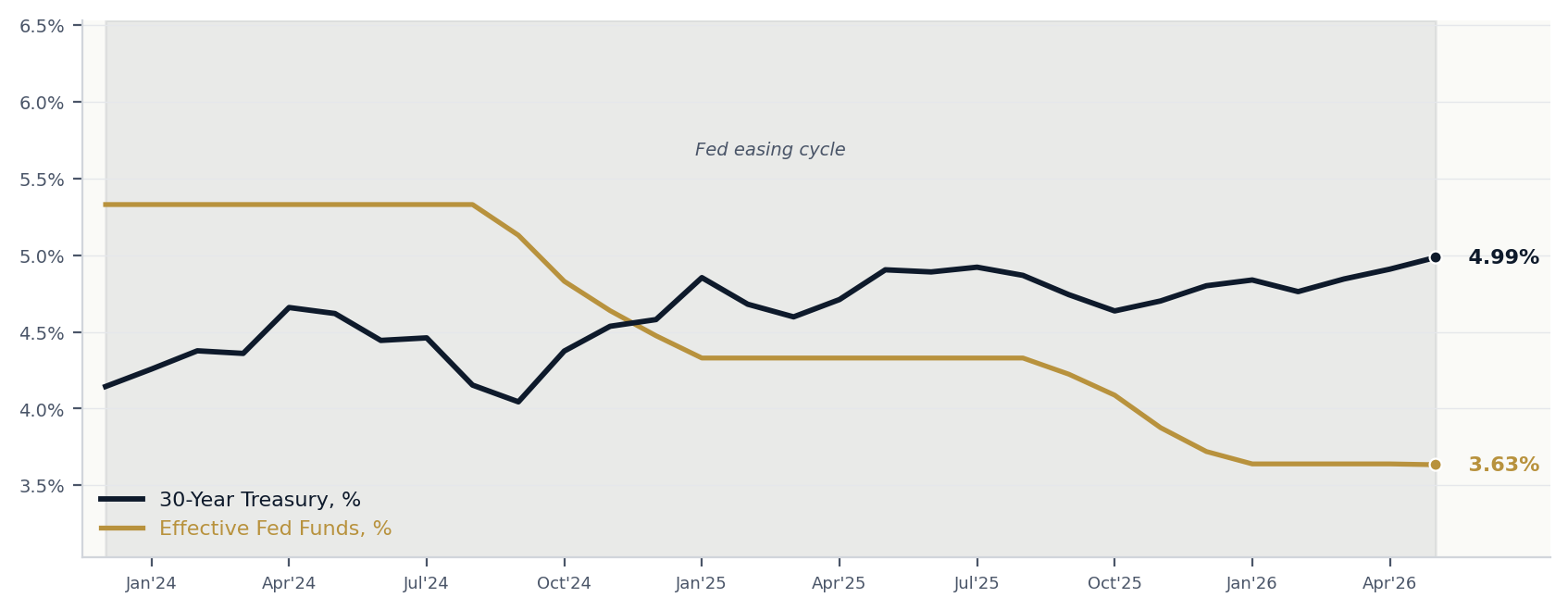

The chart below shows the structural inheritance: 175 basis points of front-end Fed cuts moved the 30-year yield by roughly 35 basis points across the entire easing cycle. A hard-money chair does not, by communication alone, close that disconnect.

30-Year Treasury vs Effective Fed Funds, 30-month window. Source: U.S. Treasury / Federal Reserve via FRED (DGS30, DFF).

FO One-Line View

The 54–45 Warsh confirmation is a regime-change event the market has priced as a personnel headline. The reconciliation runs through 17 June communication, the 2-year repricing in the interim, and the inflation-pipeline translation through summer CPI. Position into the gap, not around it.