Why April PPI Is a Services-Led Acceleration the Fed Cannot Cool with the Levers It Holds

Free Brief + Premium Edition Below

DESK

Global Macro | Inflation, Rates & Fed Policy

CONVICTION

High — structural pipeline inflation, not transitory

HORIZON

1 – 3 quarters

DATE

13 May 2026

CLASSIFICATION

Free Brief + Premium | FO Research

Executive Summary

A Pipeline Event, Not an Energy Spike

The April US Producer Price Index for final demand rose 1.4% month-on-month — the largest monthly advance since March 2022 and roughly three times the +0.5% consensus. The consensus interpretation attributes the print to gasoline and an external supply shock. The composition of the report tells a different story.

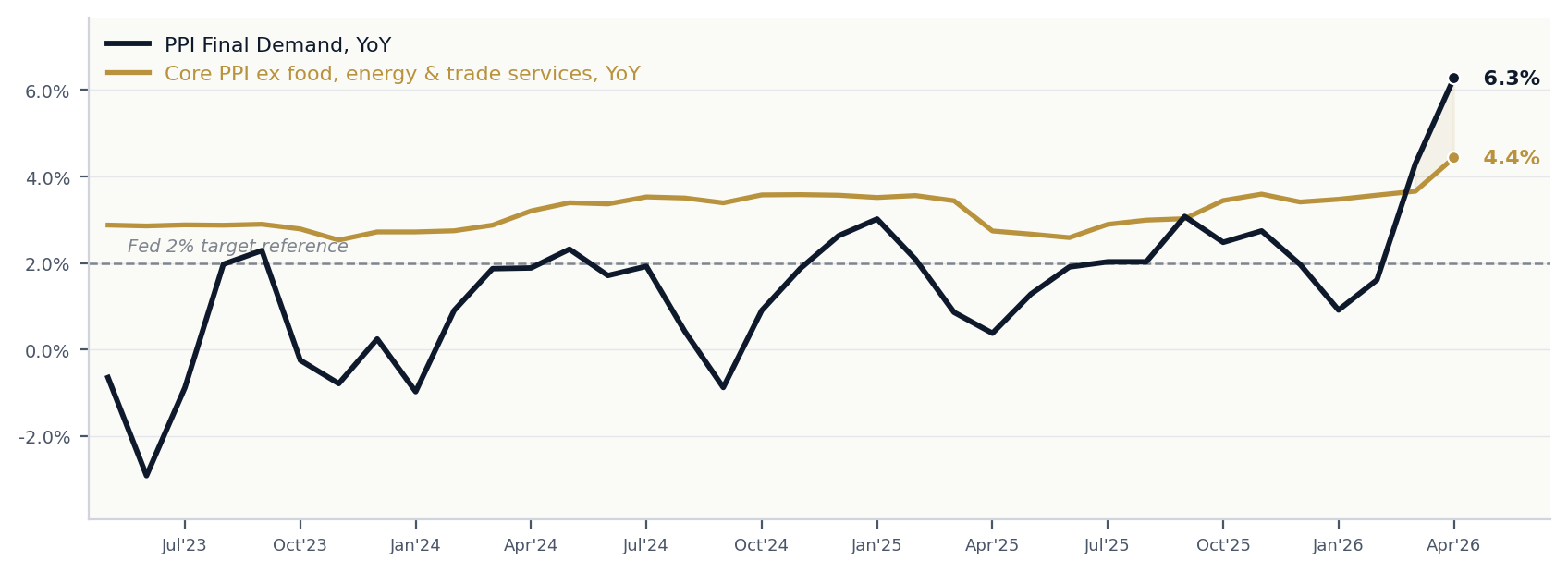

Services led the increase, contributing roughly 60% of the headline rise. Core producer prices excluding food, energy and trade-services margins accelerated to a 4.4% annual pace — the highest reading since February 2023. Stage-one intermediate demand — the input layer feeding finished-goods prices roughly 60 – 90 days downstream — rose 2.1%. None of those lines are an energy story.

The chart below shows the 12-month change in headline PPI Final Demand against the core series that excludes food, energy and trade-services margins. If the print were a pure energy event, the core line would be flat. It is not — both indices are running at the firmest pace in roughly three years.

PPI Final Demand vs Core PPI ex food, energy and trade services, year-on-year change. Source: U.S. Bureau of Labor Statistics via FRED (WPSFD49207, WPSFD49116).

FO One-Line View

April PPI is a services-led, pipeline-driven inflation event with an energy modifier — not the energy story the headline frames. The translation window to the consumer print is the June – July CPI sequence, landing on a new Fed chair with no clean path remaining.