Why the March Retail Beat Is a Fuel-Price Effect — and What Sits Below the Aggregate

Free Brief + Premium Edition Below

DESK

Global Macro | US Consumer & Equities

CONVICTION

High — structural consumer-discretionary risk

HORIZON

2 – 3 quarters

DATE

9 May 2026

CLASSIFICATION

Free Brief + Premium | FO Research

Executive Summary

The Aggregate Is Hiding the Tail

The March US retail-sales print rose 1.7%, comfortably above consensus. The street took it as constructive on consumer resilience. Strip out the gas-station receipts that account for most of the increase and real personal consumption rose 0.2%. The aggregate is a fuel-price pass-through. The underlying consumer is not the story the headline tells.

The 15.5% month-on-month jump in gas-station receipts is the dominant driver of the headline beat — that category mechanically passes higher pump prices through to nominal retail sales without any real-volume increase. Households spent more dollars in March; they bought less.

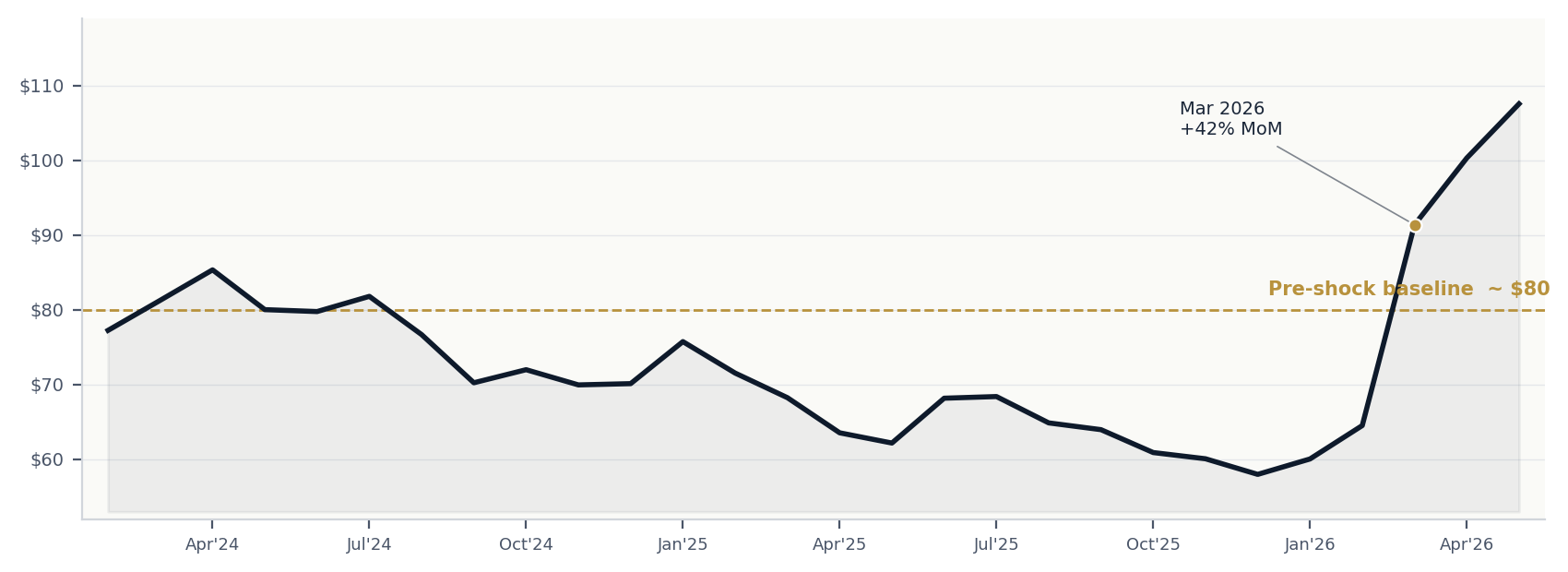

The chart below shows the WTI monthly path that has driven the gasoline pulse and the retail-sales headline.

WTI monthly average — the energy pulse running through gas-station receipts and the March retail headline. Source: U.S. EIA via FRED (DCOILWTICO).

FO One-Line View

March’s nominal retail beat is a fuel-price pass-through, not a consumption signal. The real consumer story is an income tail running at the financial margin with the Q3 federal student-loan collection restart as the catalyst markets have not yet priced.