research

Why the U.S. Dollar Could Stay Stronger for Longer

FO Research / Macro

Why the U.S. Dollar Could Stay Stronger for Longer

A Structural Reading of Yield Differentials, Relative Growth & Policy Divergence

Free Brief + Premium Edition BelowExecutive Summary

The Asymmetry Favours the Dollar

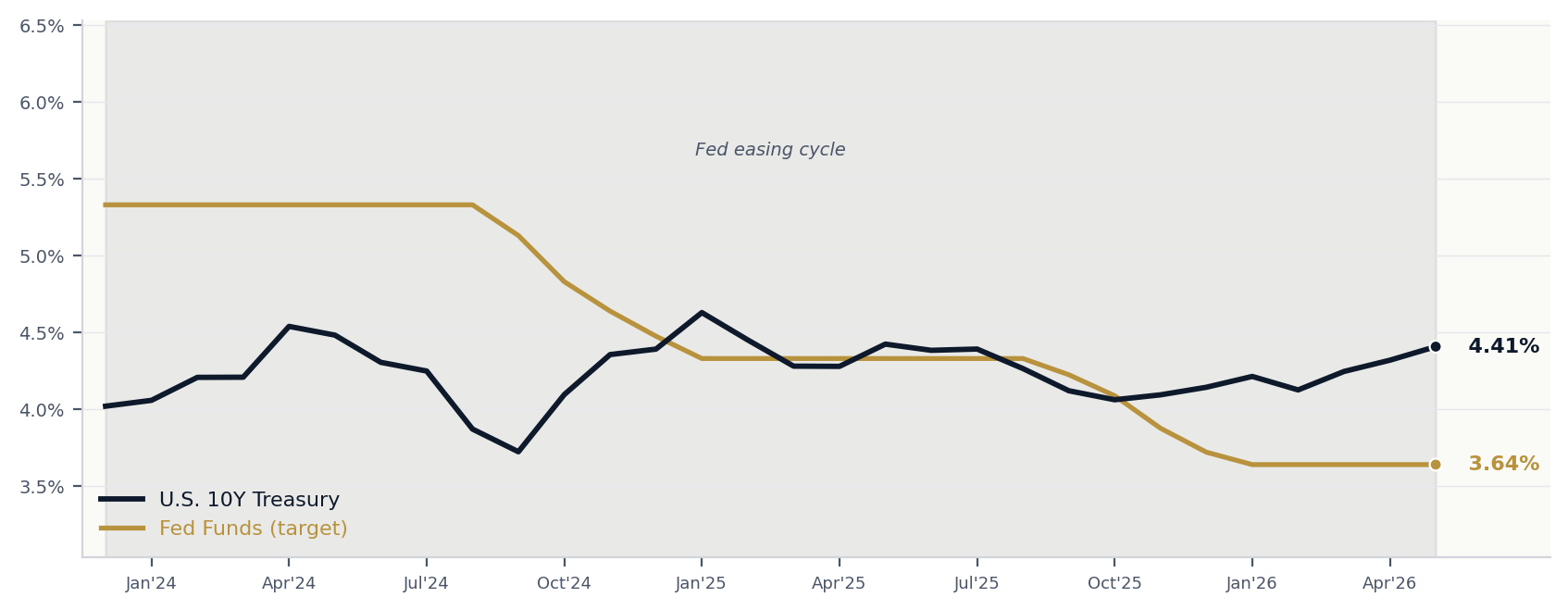

Markets continue to price a softer Federal Reserve path than current macro conditions justify. The dominant consensus narrative remains eventual rate cuts, lower Treasury yields, easier financial conditions, and a weaker U.S. dollar. When sentiment is stripped away and the underlying structure assessed, the case for continued dollar resilience remains materially stronger than many participants appreciate.

The single most important driver is the yield differential. If the Fed keeps policy restrictive while the ECB, BoE, BoJ and PBoC remain growth-constrained or move toward easing, U.S. cash and bond yields stay relatively attractive. Even if the Fed does not hike again, simply not cutting can be bullish USD if the rest of the world slows faster.

The chart below tells the story: the 10-year Treasury yield has held above the consensus easing path through every Fed meeting since the cutting cycle began. The market keeps trying to fade restrictive policy. The policy keeps proving sticky.

Receive every report at the source.

The FO Brief is free. Premium delivers the full archive. Institutional includes analyst Q&A.

Subscribe →