research

FO Market Breakdown — Dollar Strength, Oil Inflation & Higher-for-Longer Rates

FO / Market Breakdown

Dollar Strength, Oil Inflation & Higher-for-Longer Rates

An Institutional Read on the Macro Forces Shaping USD Positioning

Free Brief + Premium Edition BelowCore FO View

The Macro Stays Tilted Pro-Dollar

The market remains caught between two competing forces: strong earnings momentum on one side, and a renewed inflation impulse from oil, geopolitics, and sticky rates on the other. This week's breakdown leans toward a constructive USD bias, particularly against currencies more exposed to weaker growth, energy-import pressure, or softer central-bank credibility.

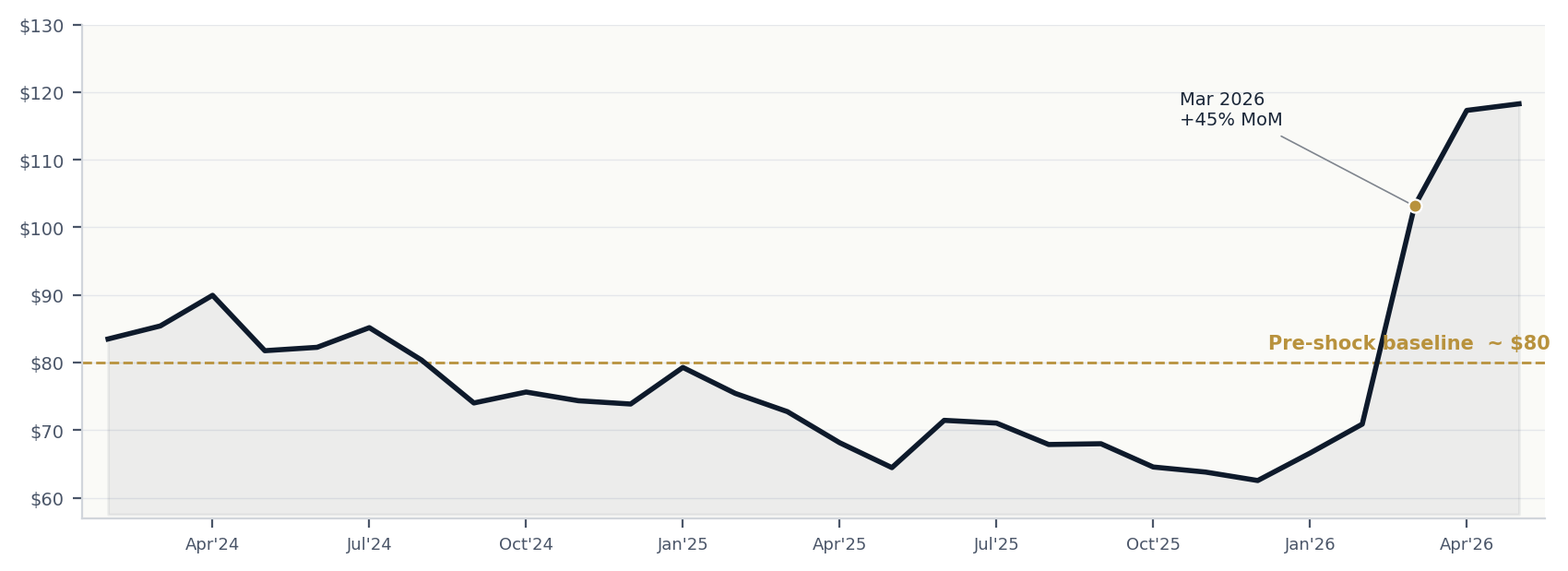

The renewed surge in oil is the central development. Reuters reported Brent crude above $111 and U.S. crude around $100, with energy supply concerns linked to the ongoing Iran conflict and Strait of Hormuz disruption. This is no longer just a fuel-pump story — it is a broader inflation transmission story. Higher crude feeds into freight, airline fares, food packaging, plastics, household goods, pharmaceuticals and business input costs, creating a second-round inflation risk that delays the Fed.

The chart below shows the Brent spike — the inflation pressure point that keeps the Fed cautious and the dollar bid.

FO Premium Edition

The Read in Full

Inflation data, labour-market context, USD-driver matrix, equity bifurcation, the desk's calibrated FX reads, scenario mapping, and the trading watchlist for the week — for Premium subscribers.

02 / Inflation Data

U.S. Inflation Data Supports Fed Caution

The latest U.S. CPI data already showed inflation pressure reaccelerating. The Bureau of Labor Statistics reported CPI rose 0.9% month-on-month in March, after rising 0.3% in February, with annual CPI at 3.3%. Core CPI rose 0.2% on the month, while airline fares rose 2.7% and apparel rose 1.0%.

That is not the type of inflation backdrop that gives the Fed room to cut aggressively. The market wants rate relief, but the data is not clean enough. If energy remains high into the next CPI cycles, the Fed will likely prefer to stay restrictive rather than risk cutting into a renewed inflation impulse — supportive of the dollar.

03 / Labour Market

Not Weak Enough for a Fed Pivot

The labour market is not collapsing. March payrolls increased by 178,000, and the unemployment rate was 4.3%, according to the latest BLS employment report. This gives the Fed breathing room.

If inflation is rising and employment is still holding, the Fed has less pressure to cut. A weak labour market would force the easing discussion; a resilient one allows the Fed to wait. For FX, the dollar performs well when the U.S. retains both:

- Relatively strong growth.

- Relatively high yields.

This is the classic dollar-supportive mix.

04 / Dollar Strength Drivers

Why the USD Remains Supported

The dollar does not need perfect U.S. data to strengthen. It only needs the U.S. to look better than the alternatives. This week the USD has three major supports:

| Driver | Read |

|---|---|

| Higher relative yields | If markets reduce rate-cut expectations, U.S. front-end yields remain attractive versus Bunds, Gilts and JGBs. Reserve managers and institutional cash continue to seek the U.S. curve. |

| Safe-haven demand | Geopolitical risk supports USD liquidity demand, particularly when oil and equities become unstable. The world's deepest liquidity pool absorbs flight-to-safety flows even when yields fall. |

| Relative resilience | U.S. labour market remains firm enough to prevent an immediate Fed pivot. Europe and Japan are more energy-import-exposed; their growth absorbs more of the oil shock. |

Reuters noted the dollar has benefited from safe-haven flows during recent hostilities, even while remaining sensitive to peace-deal headlines and month-end flows. The tactical read is therefore not "straight-line dollar bull" — it is buy-the-dip USD bias while inflation and geopolitical risk remain unresolved.

What would change our view

- Decisive oil reversal — Brent collapsing back to the pre-shock baseline on a credible diplomatic breakthrough or supply restoration. Removes the inflation-channel support for the dollar.

- U.S. labour market deterioration — payrolls turning negative or unemployment ticking decisively higher. Forces the Fed to prioritise the easing discussion over inflation risk.

- Coordinated FX intervention — credible BoJ + ECB + MoF action on excessive USD strength. Tactically caps the trade even if the underlying drivers persist.

05 / Oil

The Key Macro Trigger

Oil is now the pressure point for the entire macro board. If crude remains elevated, the market may need to reprice:

- Fewer Fed cuts.

- Higher inflation expectations.

- Stronger USD.

- Weaker risk assets.

- Pressure on energy-importing economies.

- Renewed stagflation concern.

Reuters reported oil rising sharply on disrupted supply, while equities weakened and the dollar rose on safe-haven demand. The combination is important:

Oil up + yields sticky + risk sentiment weaker = USD supportive.

06 / Equity Market

Earnings Strong, But Rate Ceiling Remains

U.S. equities have shown resilience, helped by earnings momentum and mega-cap technology expectations. Reuters noted that stocks have absorbed higher oil, higher yields, and reduced rate-cut expectations better than many anticipated.

The FO view is that the market is now walking a tighter path. Equities can continue higher if earnings remain strong, but the valuation tailwind from falling rates is missing. If inflation reaccelerates and yields rise, long-duration growth becomes more vulnerable — creating a two-speed market:

- Quality earnings and pricing power can still perform.

- Speculative long-duration growth becomes more fragile.

- Energy and defensive cash-flow names may outperform.

- Broad index upside becomes harder without lower yields.

The market can stay bid, but the risk-reward becomes more selective.

07 / FX Pair Breakdown

Tactical Read by Pair

EUR / USD

Vulnerable if energy pressure weighs more heavily on Europe than the U.S. Europe is more exposed to imported energy shocks and weaker industrial sensitivity. With U.S. yields supported and European growth weakening, rallies should struggle.

FO Bias: Sell rallies unless price confirms sustained strength above key resistance.

GBP / USD

Sterling may hold up better than EUR at times, but the UK remains vulnerable to inflation pressure, consumer squeeze, and growth fragility. Broad USD strength caps upside; BoE is reactive rather than proactive in the current rate mix.

FO Bias: Neutral-to-bearish on rallies. Watch UK inflation and BoE tone.

USD / JPY

Driven by yield differentials. With U.S. yields elevated and the BoJ cautious, the pair remains supported. Reuters noted the yen weakened after the BoJ left rates unchanged at 0.75%. Carry remains tilted structurally toward USD; intervention risk is the only meaningful counterweight near term.

FO Bias: Buy dips while U.S. yields remain firm — manage intervention risk.

AUD / USD

Exposed to risk sentiment and China / global growth. Higher oil can lift commodity FX, but AUD usually struggles when risk appetite deteriorates and USD safe-haven demand rises. Iron-ore and metals leadership matters less than risk-sentiment direction in this regime.

FO Bias: Bearish if equities weaken and China momentum remains soft.

NZD / USD

More vulnerable than AUD in a risk-off USD environment — less commodity insulation and remains sensitive to global liquidity. Carry trades unwind first when volatility expands.

FO Bias: Bearish while USD momentum and risk-off flows persist.

USD / CAD

CAD has oil support, but the pair depends on whether oil strength benefits Canada more than it strengthens USD via inflation and Fed repricing. Supply-driven crude rallies (the current regime) can keep USD on top because the inflation channel dominates the commodity channel.

FO Bias: Mixed. Prefer trading levels rather than chasing.

Gold

Caught between two forces — geopolitical fear supports safe-haven demand, while higher yields and USD strength pressure non-yielding assets. Aggressive real-yield rises may pressure gold; sharp geopolitical escalation can decouple it from the USD trade.

FO Bias: Neutral-to-bullish on escalation; cautious if yields and USD rise together.

Oil

Brent above $100 keeps inflation anxiety alive and makes central-bank easing harder. If supply disruption remains unresolved, oil strength becomes a direct input into USD strength via Fed repricing — the second-order channel.

FO Bias: Bullish while disruption risk remains unresolved — headline-sensitive.

08 / Scenario Map

Three Forward Paths

| Scenario | Trigger | Likely market reaction |

|---|---|---|

| 1. Bullish USD / Bearish Risk Base case | Oil stays elevated through the Strait of Hormuz disruption window; CPI pressure builds in next prints; Fed holds restrictive. | DXY higher; U.S. yields firm; EUR/USD lower; GBP/USD capped; AUD/NZD weaker; equities more selective with energy / quality leadership; gold mixed on yield-vs-fear tug. |

| 2. Peace Deal / Oil Reversal Lower probability | Geopolitical tension eases via diplomatic breakthrough; oil falls sharply on supply-restoration headlines; risk-on rotation. | USD softens; yields fall; EUR/USD and GBP/USD rebound; AUD/NZD recover; equities rally; gold may fade as real-rate cover returns. |

| 3. Stagflation Shock Tail risk | Oil stays high while U.S. growth slows; CPI prints surprise to the upside as labour softens; Fed trapped between mandates. | USD stronger as safe haven; equities under pressure; gold supported on risk fear and policy-credibility concern; bonds volatile; high-beta FX underperforms; central banks remain trapped. |

09 / FO Trading Focus

Watchlist for the Week

The main trade theme is to avoid blindly shorting USD unless the data clearly turns against it. Watch:

- Crude oil holding above key levels.

- U.S. CPI and inflation expectations.

- Fed communication and dot-plot evolution.

- Treasury yield reaction across the curve.

- Equity market breadth versus mega-cap leadership.

- EUR/USD rejection zones.

- AUD/NZD risk-sentiment breakdowns.

- USD/JPY yield sensitivity and intervention skews.

Strong oil + sticky inflation + resilient jobs = Fed delay = USD support.

FO Closing View

The Path of Least Resistance Favours the Dollar

The market still wants to believe in rate cuts, but the macro backdrop is becoming less friendly for that view. Oil is rising, inflation is sticky, the labour market is not weak enough, and geopolitical risk remains active. That combination keeps the Fed cautious and keeps the dollar supported.

Until oil reverses sharply or U.S. data deteriorates meaningfully, USD weakness should be treated carefully — the better probability is that the dollar stays bid on dips, particularly versus currencies with weaker growth, higher energy sensitivity, or lower yield support.

Receive every report at the source.

The FO Brief is free. Premium delivers the full archive. Institutional includes analyst Q&A.

Subscribe →