The Rating Agency Put Letterhead on a Verdict the Market Had Already Reached

Free Brief + Premium Edition Below

DESK

Global Macro | Rates & Fixed Income

CONVICTION

High · structural, now agency-ratified

HORIZON

2 to 4 quarters

DATE

19 May 2026

CLASSIFICATION

Free Brief + Premium | FO Research

Executive Summary

A Verdict the Market Reached First

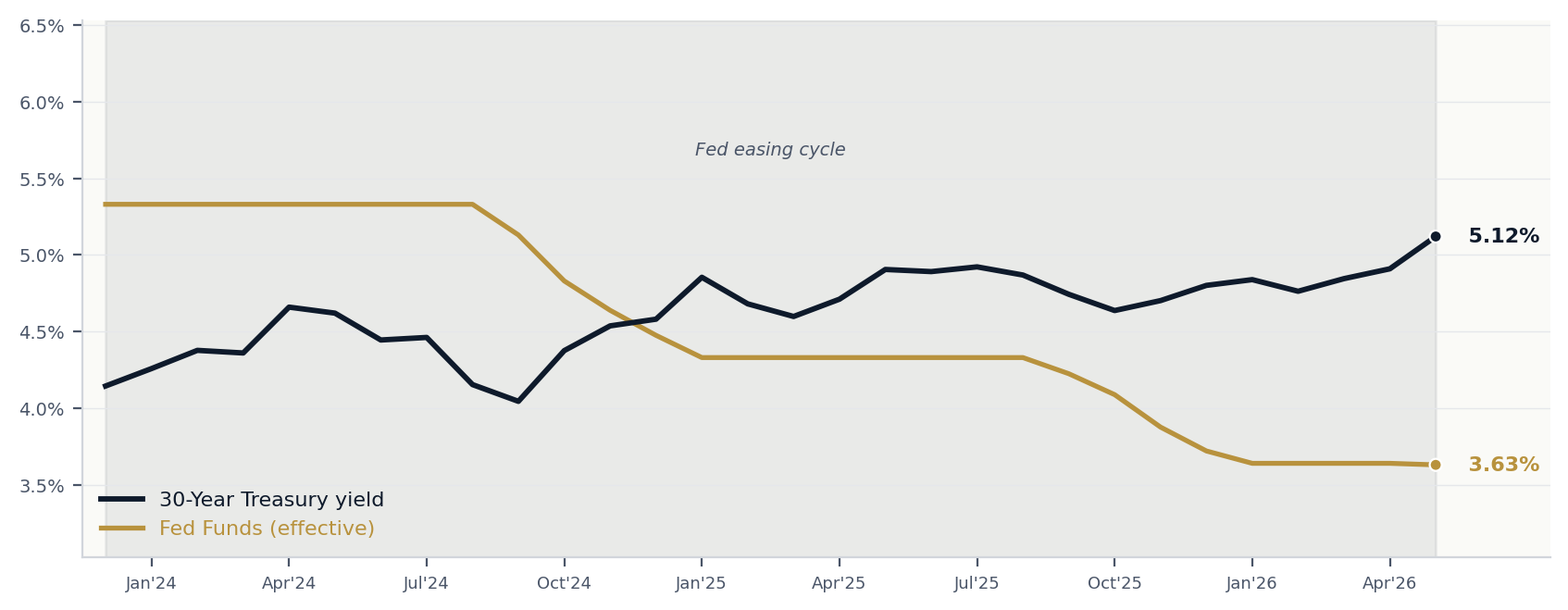

On 16 May 2026 the United States lost its last top-tier sovereign credit rating. The cut was one notch. The significance is not the notch. It is that, for the first time, all three major rating agencies now hold the United States below the top tier simultaneously. The headline you will have read is that the reaction was muted. That framing makes a category error: it assumes the bond market reacted to the announcement. It did not. The market spent the week building the verdict one auction and one print at a time. By the prior session’s close the 30-year was already at 5.12% and the 10-year at 4.59%. The agency did not move the market. It ratified where the market had already gone.

We called the structural long-end disconnect on 8 May. The rating action is the institutional ratification of that thesis, not a new one. The forward leg it activates, the part the consensus is not pricing, is the mandate channel: the marginal, price-insensitive, mandate-constrained buyer of size now has a technical reason to step back, independent of view.

The chart below is the disconnect in one line: 175 basis points of front-end cuts across the easing window, and the 30-year did not follow it down. It has pushed through 5%. The rating action did not create that gap. It named it.

30-Year Treasury vs Effective Fed Funds, daily, 30-month window. Source: U.S. Treasury / Federal Reserve via FRED (DGS30, DFF).

FO One-Line View

The downgrade did not cause the sell-off. It ratified the structural long-end disconnect we published on 8 May. The forward leg is the mandate channel: a contracting pool of price-insensitive holders, playing out over quarters in the slow data, not in a single session.